All Categories

Featured

Table of Contents

Juvenile insurance coverage may be sold with a payor advantage biker, which offers for forgoing future costs on the kid's plan in case of the fatality of the person who pays the costs. best term life insurance with living benefits. Senior life insurance policy, often referred to as graded fatality advantage strategies, gives qualified older candidates with very little whole life insurance coverage without a medical exam

The permissible problem ages for this kind of coverage array from ages 50 75. The optimum problem amount of protection is $25,000. These plans are usually much more expensive than a completely underwritten plan if the individual qualifies as a conventional threat. This sort of protection is for a small face amount, normally bought to pay the funeral expenses of the insured.

You choose to obtain one year of highly economical insurance coverage so you can make a decision if you want to devote to a longer-term plan.

The Federal Government developed the Federal Employees' Team Life Insurance Policy (FEGLI) Program on August 29, 1954. It is the biggest group life insurance coverage program in the world, covering over 4 million Federal staff members and retirees, along with a lot of their family participants. A lot of staff members are qualified for FEGLI coverage.

Term Vs Universal Life Insurance

As such, it does not develop any kind of money value or paid-up value. It includes Fundamental life insurance policy protection and 3 options. In many cases, if you are a new Federal employee, you are automatically covered by Standard life insurance policy and your pay-roll office subtracts premiums from your paycheck unless you forgo the coverage.

You have to have Basic insurance policy in order to choose any of the options. The cost of Fundamental insurance policy is shared in between you and the Federal government.

You pay the complete cost of Optional insurance, and the price depends on your age. The Office of Federal Worker' Group Life Insurance Coverage (OFEGLI), which is a personal entity that has an agreement with the Federal Government, procedures and pays cases under the FEGLI Program.

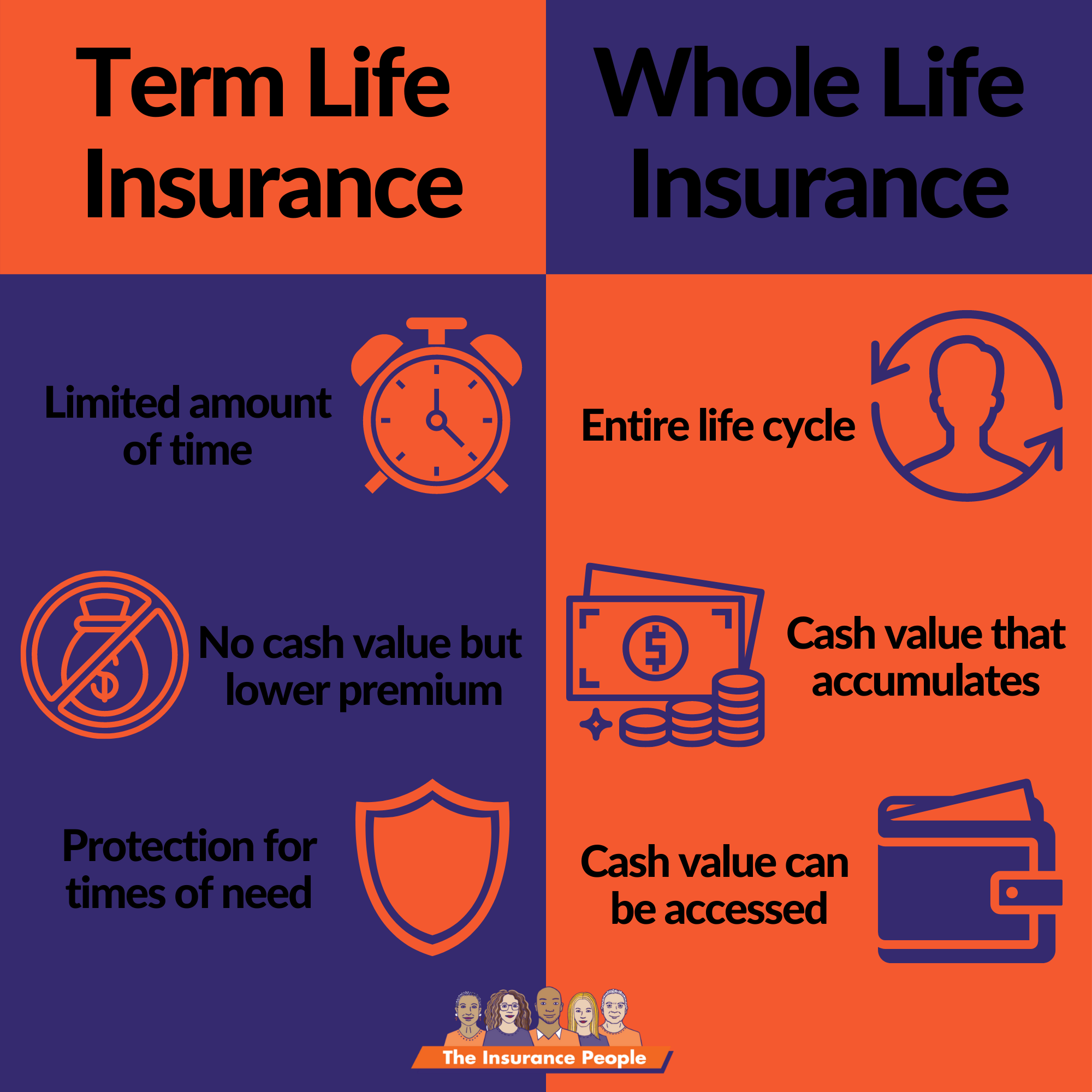

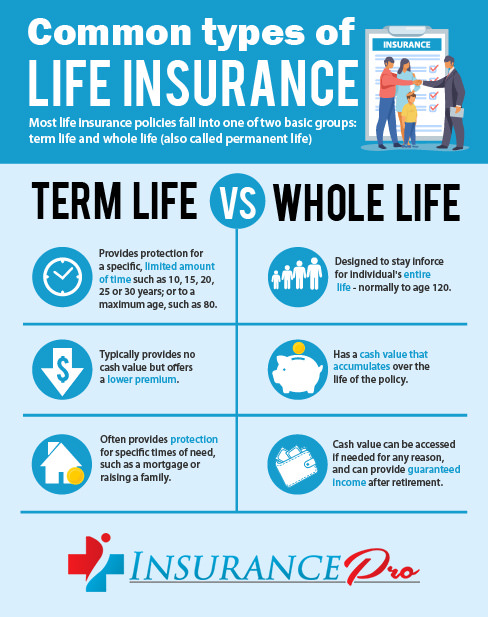

Term life insurance coverage is a kind of life insurance policy that gives insurance coverage for a certain duration, or term, chosen by the insurance holder. It's typically the most uncomplicated and budget friendly life insurance policy choice by covering you for a set "term" (life insurance policy terms are usually 10 to thirty years). If you pass away throughout the term period, your beneficiaries receive a cash money payment, called a survivor benefit.

Term life insurance is an uncomplicated and economical remedy for individuals looking for inexpensive protection during particular durations of their lives. It is essential for people to carefully consider their financial objectives and needs when picking the period and amount of protection that ideal matches their conditions. That claimed, there are a few reasons that lots of people select to get a term life plan.

This makes it an eye-catching alternative for people who desire significant insurance coverage at a lower price, especially throughout times of higher financial duty. The other crucial benefit is that costs for term life insurance plans are taken care of throughout of the term. This implies that the policyholder pays the very same costs quantity every year, offering predictability for budgeting objectives.

What Is A Level Term Life Insurance Policy

2 Expense of insurance prices are figured out using approaches that vary by firm. It's important to look at all aspects when reviewing the overall competition of rates and the worth of life insurance policy protection.

Nothing in these products is intended to be guidance for a certain circumstance or person. Please seek advice from your own advisors for such guidance. Like most group insurance plan, insurance coverage supplied by MetLife contain specific exclusions, exemptions, waiting durations, reductions, restrictions and terms for keeping them active. Please call your benefits administrator or MetLife for expenses and full details.

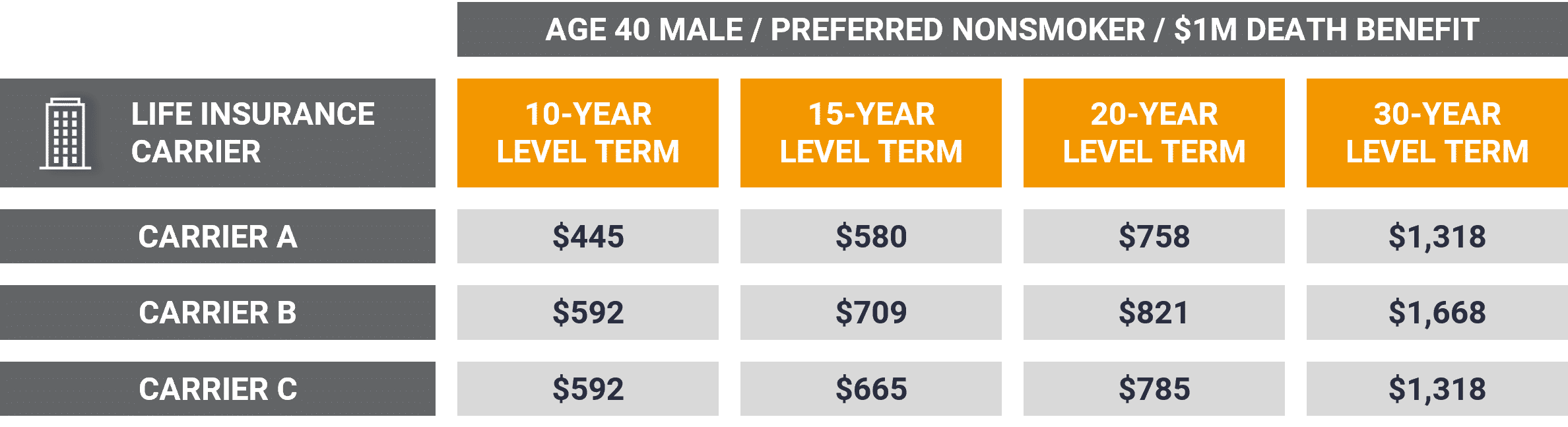

Our term life options include 10, 15, 20, 25, 30, 35, and 40-year plans. The most prominent type is level term, implying your repayment (premium) and payout (survivor benefit) stays degree, or the same, until completion of the term duration. This is the most uncomplicated of life insurance policy alternatives and requires extremely little maintenance for plan owners.

As an example, you could give 50% to your partner and divided the remainder among your adult children, a moms and dad, a good friend, and even a charity. * In some circumstances the fatality advantage may not be tax-free, discover when life insurance coverage is taxable.

Term life insurance policy offers coverage for a details amount of time, or "term" of years. If the guaranteed individual passes away within the "term" of the plan and the plan is still effective (energetic), then the survivor benefit is paid to the beneficiary. voluntary term life insurance meaning. This kind of insurance coverage typically allows clients to originally buy even more insurance coverage for much less cash (premium) than various other type of life insurance policy

Life insurance acts as a substitute for income. The prospective danger of losing that making power profits you'll require to fund your family's most significant objectives like purchasing a home, paying for your children' education, lowering financial debt, saving for retired life, and so on.

Living Benefits Term Life Insurance

Term life is the simplest type of life insurance. It supplies a pure death advantage. The plan will cover the guaranteed for a given period of time (the "term"), such as 10 or 20 years, or up until a defined age. If you purchase term life insurance policy at a more youthful age, you can usually buy even more at a lower price.

Term insurance policy is preferably matched to cover certain needs that may lower or vanish over time Following are 2 usual stipulations of term insurance coverage you might wish to take into consideration throughout the purchase of a term life insurance policy. enables the insured to renew the policy without needing to verify insurability.

Before they offer you a plan, the supplier requires to evaluate just how much of a threat you are to insure. This is called the "underwriting" procedure. They'll typically request a medical examination to assess your wellness and want to understand even more about your line of work, way of living, and other things. Particular leisure activities like diving are deemed risky to your health and wellness, and that might raise rates.

The Cost Of 500 000 Worth Of 30-year Term Life Insurance For Fernando

The costs related to term life insurance costs can vary based upon these variables - which of the following is not a characteristic of term life insurance. You need to pick a term length: One of the biggest concerns to ask on your own is, "Exactly how long do I need coverage for?" If you have youngsters, a prominent general rule is to select a term long sufficient to see them away from the house and with university

1Name your beneficiaries: Who gets the advantage when you pass away? It doesn't all need to go to one individual. For instance, you can provide 50% to your spouse and divide the remainder in between your adult children. And while beneficiaries are typically household, they don't need to be. You can choose to leave some or all of your advantages to a trust fund, a charitable company, and even a buddy.

Consider Making use of the dollar formula: penny stands for Financial debt, Revenue, Home Loan, and Education and learning. Total your financial obligations, home loan, and college expenses, plus your wage for the number of years your family needs security (e.g., until the kids are out of your home), which's your insurance coverage demand. Some financial professionals compute the amount you require utilizing the Human Life Value philosophy, which is your lifetime revenue potential what you're gaining currently, and what you expect to make in the future.

One means to do that is to look for business with strong Monetary toughness ratings. 8A business that underwrites its own plans: Some firms can offer policies from an additional insurance firm, and this can add an extra layer if you intend to transform your policy or later on when your family needs a payout.

Some business offer this on a year-to-year basis and while you can expect your prices to increase significantly, it may be worth it for your survivors. One more method to contrast insurance business is by looking at on-line client evaluations. While these aren't most likely to tell you much regarding a firm's economic security, it can tell you just how simple they are to work with, and whether cases servicing is an issue.

Is Voluntary Term Life Insurance Worth It

When you're more youthful, term life insurance policy can be a basic means to secure your enjoyed ones. As life adjustments your economic top priorities can as well, so you may want to have entire life insurance policy for its life time insurance coverage and added benefits that you can use while you're living. That's where a term conversion is available in.

Authorization is ensured despite your wellness. The costs won't boost when they're established, yet they will certainly increase with age, so it's a good concept to lock them in early. Figure out even more concerning exactly how a term conversion works.

1Term life insurance coverage offers short-term defense for a crucial duration of time and is usually more economical than long-term life insurance policy. 2Term conversion guidelines and limitations, such as timing, might apply; for instance, there might be a ten-year conversion benefit for some products and a five-year conversion privilege for others.

3Rider Insured's Paid-Up Insurance Purchase Choice in New York. There is a cost to exercise this rider. Not all participating policy owners are eligible for rewards.

{kind=link}

Latest Posts

What Is Short Term Life Insurance

Term Life Insurance Icon

Child Rider Term Life Insurance